Can a lender require credit life insurance

4. Some lenders require credit life insurance. This usually occurs with mortgage loans in which the borrower is putting down less than 20 percent of the loan value. A few years down the line, when the borrower owns more equity in the home, the lender may consider a borrower’s request to cancel the policy.

Is credit life insurance mandatory?

Credit life cover is not always compulsory To protect consumers, the National Credit Regulator (NCR) implemented rules that govern mandatory credit insurance agreements. … While some credit insurance providers do provide the option of including the unemployment or unable to earn an income benefit, this is not widespread.

Can a bank require life insurance?

Many banks now require life insurance coverage on borrowers, and possibly on guarantors as well. It’s a sensible form of collateral and protection for the bank and is not a new practice at all. In fact, it used to be common for lenders to require life insurance coverage on borrowers.

Is it prohibited for a creditor to require credit insurance?

When you take out a loan, or when you use a credit card, you have the option of purchasing credit insurance. … In fact, the Federal Trade Commission (FTC) has stated that that it’s illegal for a lender to deceptively include insurance or other optional products in your loan without your knowledge or permission.Why are borrowers often required to purchase credit life and disability insurance?

They want to keep the property securing the loan. If the value of your estate isn’t large enough to cover the outstanding loan on your car or home, your family would need to pay off the debt in order to keep the property.

What are the three types of credit insurance?

There are three kinds of credit insurance—disability, life, and unemployment—available to credit card customers.

Who pays premiums for a credit life insurance policy?

In a typical policy, the borrower will pay a premium — often rolled into their monthly loan payment — that allows the lender to be paid in full if the borrower dies before paying off the loan.

When making a credit decision a lender may consider?

Capacity. Lenders need to determine whether you can comfortably afford your payments. Your income and employment history are good indicators of your ability to repay outstanding debt. Income amount, stability, and type of income may all be considered.Do lenders have to tell you why you are denied credit?

If a lender rejects your application, it’s required under the Equal Credit Opportunity Act (ECOA) to tell you the specific reasons your application was rejected or tell you that you have the right to learn the reasons if you ask within 60 days.

When evaluating a credit request a lender may consider?When determining a consumer’s creditworthiness, financial institutions must instead consider income, expenses, debts and credit history. Creditors are permitted to ask for certain information to help in the documentation process, but even that is limited by certain rules.

Article first time published onDo banks accept life insurance as collateral?

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. A permanent life insurance policy with a cash value allows the lender access to the cash value to use as loan payment if the borrower defaults.

What type of life insurance are credit policies issued as?

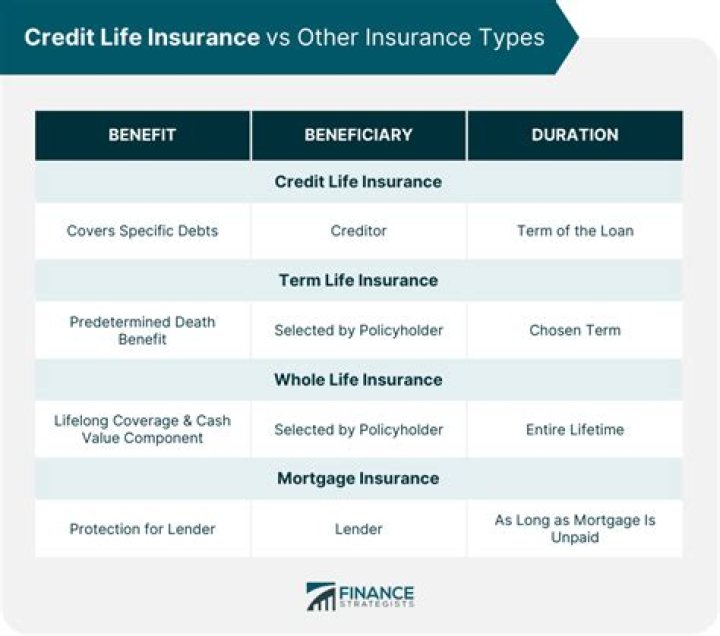

Credit life insurance is a type of life insurance policy designed to pay off a borrower’s outstanding debts if the borrower dies. The face value of a credit life insurance policy decreases proportionately with the outstanding loan amount as the loan is paid off over time, until both reach zero value.

What credit life insurance covers?

Credit life insurance is an insurance product specifically designed to cover the cost of your debt if you aren’t able to pay it back due to disability, unemployment or death. … Instead, the amount you still owe on that debt or your instalments payable will be covered by your credit life insurance.

Can you put credit life on a mortgage?

Credit life insurance can cover mortgages, auto loans, education loans, bank credit loans or other types of loans. In general, the amount of insurance can’t be more than what you owe on the loan. Your state may set maximum coverage limits for credit life insurance policies.

What is credit insurance for banks?

Credit insurance covers your loan or credit card payments in the event you become unable to pay due to a financial shock like unemployment, disability or death.

What is credit insurance on a loan?

Credit insurance is optional insurance that make your auto payments to your lender in certain situations, such as if you die or become disabled. … If you add credit insurance to your loan, this increases your loan amount and you will pay additional interest.

Who owns a credit life policy?

Who is the policy owner in credit life insurance? You are the owner of your credit life insurance policy, but the policy’s beneficiary is your lender, rather than beneficiaries of your choosing.

How do I find out if someone has life insurance on my credit?

Visit NAIC.org and you can find your state’s insurance department’s contact information. While you’re there check out their free policy locator tool. If your loved one had a life insurance policy and you’re the beneficiary, the NAIC may be able to find the information and share it with you.

Is the creditor the insured in credit life insurance?

Credit life insurance pays a policyholder’s debts when the policyholder dies. Unlike term or universal life insurance, it doesn’t pay out to the policyholder’s chosen beneficiaries. Instead, the policyholder’s creditors receive the value of a credit life insurance policy.

What are the things you need to consider before purchasing credit insurance?

- Shop around. …

- Only buy insurance to maintain your existing standard of living. …

- Ask your insurance provider what the policy doesn’t cover. …

- Consider bundling several policies with one insurance carrier. …

- Review your insurance needs on a yearly basis.

What is most likely to cause a lender to deny credit?

Two primary factors lead lenders to deny loan applications: problems with credit and problems with income. In some situations, however, other factors may also contribute to the decision.

How can I build credit if I can't get approved for anything?

- Become an authorized user. One of the simplest ways to build credit is by becoming an authorized user on a family member or friend’s credit card. …

- Apply for a secured credit card. …

- Get credit for paying monthly utility and cell phone bills on time.

What two things should you do if your lender rejects your loan application?

- Prequalify With Other Lenders. Since different lenders have different lending requirements, try prequalifying with other lenders. …

- Provide Collateral. …

- Request a Lower Loan Amount. …

- Increase Your Down Payment Amount.

What are the only three reasons a creditor may deny credit?

Low credit score, too many late payments on accounts, too many accounts in collection status, high debt to income ratio, credit history too short (meaning you haven’t had accounts long enough to establish good credit), your income is unstable, you have too many open credit cards, you have too many hard credit inquiries …

What are 5 C's of credit?

Understanding the “Five C’s of Credit” Familiarizing yourself with the five C’s—capacity, capital, collateral, conditions and character—can help you get a head start on presenting yourself to lenders as a potential borrower. Let’s take a closer look at what each one means and how you can prep your business.

Which of the following prohibited factors Cannot be used when making credit decisions?

Prohibited bases: race, color, religion, national origin, sex, marital status, age (provided the applicant has capacity to contract), receipt of public assistance, or exercise of rights under the Consumer Credit Protection Act.

Why should a company use the credit evaluation?

The business credit score is a measure of a company’s financial stability and can predict how likely they are to pay you on time.

What does the Equal credit Opportunity Act require?

This Act (Title VII of the Consumer Credit Protection Act) prohibits discrimination on the basis of race, color, religion, national origin, sex, marital status, age, receipt of public assistance, or good faith exercise of any rights under the Consumer Credit Protection Act.

What does rescission period mean?

The right of rescission refers to the right of a consumer to cancel certain types of loans. If you are refinancing a mortgage, and you want to rescind (cancel) your mortgage contract; the three-day clock does not start until. You sign the credit contract (usually known as the Promissory Note)

Can you borrow against the death benefit of a life insurance policy?

You can only borrow against a permanent or whole life insurance policy. Policy loans are borrowed against the death benefit, and the insurance company uses the policy as collateral for the loan. Life insurance companies add interest to the balance, which accrues whether the loan is paid monthly or not.

What is considered a collateral on a life insurance policy loan?

A collateral assignment of life insurance occurs when an insured uses their insurance policy as collateral for a loan. If the insured dies while the policy is in force, some or all of the death benefit may be used to pay off the loan that the insured took out.