How are mortgage prepayment penalties calculated

If you want to find out if your loan has a prepayment penalty, look at your monthly billing statement or coupon book. You can also look at the paperwork you signed at the loan closing. Usually paragraphs regarding prepayment penalties are in the promissory note or sometimes in an addendum to the note.

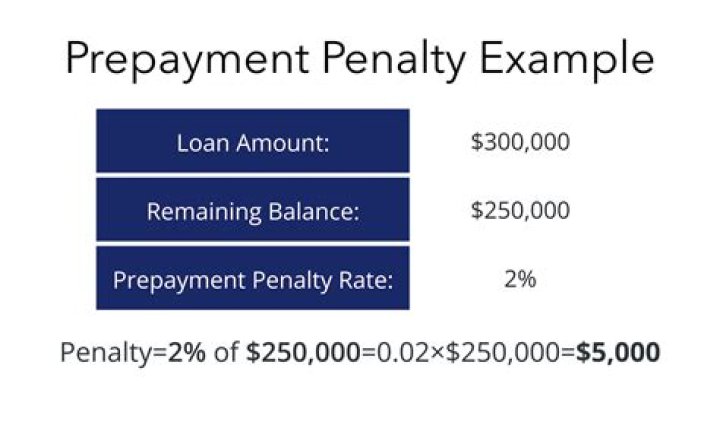

How is mortgage prepayment penalty calculated?

If you want to find out if your loan has a prepayment penalty, look at your monthly billing statement or coupon book. You can also look at the paperwork you signed at the loan closing. Usually paragraphs regarding prepayment penalties are in the promissory note or sometimes in an addendum to the note.

What is the typical prepayment penalty on a mortgage?

Prepayment penalties typically start out at around 2% of the outstanding balance if you repay your loan during the first year. Some loans have higher penalties, but many loan types are limited to 2% as a maximum. Penalties then decline for each subsequent year of a loan until they reach zero.

How do banks calculate prepayment penalty?

- the amount you want to prepay (or pay off early)

- the number of months left until the end of your term.

- interest rates.

- the method your lender uses to calculate the fee.

How is prepayment interest calculated?

In short, if you are depositing a cheque to prepay Home Loan on 15th of the particular month then your date of payment is 15th. Prepayment Interest will be calculated from 1st to 14th of the month.

What are disadvantages of principal prepayment?

- Some mortgages come with a “prepayment penalty.” The lenders charge a fee if the loan is paid in full before the term ends.

- Making larger monthly payments means you may have limited funds for other expenses. …

- You may have gotten an extremely low interest rate with your mortgage.

How are loan penalties calculated?

First, divide the annual interest rate in half to get 2.5 percent. Then, multiply this value by the outstanding balance to get interest paid in six months. This would be $150,000*0.025, or $3,750. Then, multiply this result by 80 percent to find the prepayment penalty.

Is a prepayment penalty considered interest?

Generally for a debtor, prepayment charges are deductible as interest because they are considered an additional amount paid for the use of money.How do I avoid a prepayment penalty?

Yes, you can try negotiating it down, but the best way to avoid the fee altogether is to switch to a different loan or a different lender. Since not all lenders charge the same prepayment penalty, make sure to get quotes from different lenders to find the best loan for you.

How does prepayment penalty work?A prepayment penalty clause states that a penalty will be assessed if the borrower significantly pays down or pays off the mortgage, usually within the first five years of the loan. Prepayment penalties serve as protection for lenders against losing interest income.

Article first time published onAre mortgage prepayment penalties tax deductible?

To deduct the entire prepayment penalty in one year, you must pay the penalty in full. If you refinance and roll the penalty into your new loan, you can deduct the penalty over the life of the loan. For borrowers who refinance but choose to pay the prepayment penalty at closing, the entire penalty is deductible.

Why do banks charge prepayment penalties?

In April, the Reserve Bank of India (RBI) asked banks to stop levying foreclosure charges and pre-payment penalties on floating rate home loans. The levying of these charges was seen as a restrictive practice to deter borrowers from switching to lenders offering lower rates.

Does prepayment reduce principal?

No, it actually does not. Many borrowers misunderstand that part-prepayments will reduce your EMI. … When you pay your EMI, the interest amount is deducted and the rest is paid towards the principal. Now, when you make a prepayment, the total principal outstanding is reduced.

Which is better reducing tenure or EMI?

Choosing between EMIs and tenure reductions While a reduction in the loan tenure will result in greater savings in interest pay out, opting for the EMI reduction option will lead to higher disposable income.

How much does 1 point lower your interest rate?

Each point typically lowers the rate by 0.25 percent, so one point would lower a mortgage rate of 4 percent to 3.75 percent for the life of the loan.

What is the penalty interest rate?

Penalty interest rates The current penalty interest rate was fixed by the Attorney-General under section 2 of the Penalty Interest Rate Act 1983 at 10% per annum with effect on and from 1 February 2017.

What happens if I pay an extra $1000 a month on my mortgage?

Paying an extra $1,000 per month would save a homeowner a staggering $320,000 in interest and nearly cut the mortgage term in half. To be more precise, it’d shave nearly 12 and a half years off the loan term. The result is a home that is free and clear much faster, and tremendous savings that can rarely be beat.

Why you shouldn't pay off your house early?

Paying off early means increased sequence of return risk. Paying off your mortgage early means foregoing adding more to your investment portfolio today. … But if your investment horizon is shorter, you could face several years of poor returns at the most inopportune time.

How can I pay off my 30-year mortgage in 15 years?

- Adding a set amount each month to the payment.

- Making one extra monthly payment each year.

- Changing the loan from 30 years to 15 years.

- Making the loan a bi-weekly loan, meaning payments are made every two weeks instead of monthly.

What states have no prepayment penalties?

In some cases, a prepayment penalty could apply if you pay off a large amount of your mortgage all at once. The majority of states allow prepayment penalties, however, there are some exceptions, notably Maine, Massachusetts, and Nevada.

What is a 3 2 1 prepayment penalty?

We currently offer investors the ability to pay extra basis points for a 3/2/1 prepayment structure or a 3/0/0 prepayment structure. That means if they pay off the loan in the first year, they only have a 3% penalty, and after three years, there are no penalties.

At what income level do you lose mortgage interest deduction?

There is an income threshold where once breached, every $100 over minimizes your mortgage interest deduction. That level is roughly $200,000 per individual and $400,000 per couple for 2021.

How is average mortgage balance calculated?

To figure your average balance, add the starting balance to the ending balance and divide by 2. For example, say your starting balance was $1.25 million and your ending balance was $1.15 million. Your average is $1.2 million.

Can I deduct mortgage interest in 2021?

That means this tax year, single filers and married couples filing jointly can deduct the interest on up to $750,000 for a mortgage if single, a joint filer or head of household, while married taxpayers filing separately can deduct up to $375,000 each.

Why would a bank punish you with a prepayment penalty for paying off a loan early?

Lenders make most of their profit from interest, so if you pay off your loan early, the lender is possibly losing out on the interest payments that they were anticipating. Charging a prepayment penalty is one way a lender may recoup their financial loss if you pay off your loan early.

What is a soft prepayment penalty?

A soft prepayment penalty lets you sell your home without a prepayment penalty. However, if you choose to refinance your loan, you are subject to pay a prepayment penalty. If you have a hard prepayment penalty, you could be responsible for paying the prepayment penalty, if you sell or if you refinance.

Does paying more principal reduce interest?

Save on interest Since your interest is calculated on your remaining loan balance, making additional principal payments every month will significantly reduce your interest payments over the life of the loan. By paying more principal each month, you incrementally lower the principal balance and interest charged on it.

Which is better increasing EMI or part payment?

For home loans, a higher EMI or prepayment will cut interest outgo, tenure. … And if interest rates are falling, even better. Increase EMI if you can. Higher EMIs not only help you get rid of a liability faster but also save big on interest outflow.

What happens if I pay more than EMI?

Yes, you can pay more than the regular EMI. The excess amount will not only decrease your principal outstanding, but also reduce your interest burden. You can pay one extra EMI (than the usual number of EMIs) every year. This is an effective way to reduce your loan tenure, and in turn to lower the interest cost.

What is the best tenure for home loan?

TenureMax Home Loan AmountEMI Amount20 yearsRs. 44.70 LacsRs. 36,01025 yearsRs. 48.70 LacsRs. 35,99030 yearsRs. 51.50 LacsRs. 36,010

Does PMAY reduce EMI or tenure?

Interest and EMI of the Home Loans under the PMAY The maximum tenure of the housing loans under this scheme is 20 years. The National Housing Bank will pay the entire subsidy in one go to your lender. This further reduces your EMI burden.