How do GAAP and IFRS differ in terms of the treatment of loss contingencies

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. This disconnect manifests itself in specific details and interpretations. Basically, IFRS guidelines provide much less overall detail than GAAP.

What are the main differences between IFRS and GAAP?

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. This disconnect manifests itself in specific details and interpretations. Basically, IFRS guidelines provide much less overall detail than GAAP.

What is a contingent liability How is a contingent liability reported under GAAP How does this differ under IFRS?

A contingent liability is a liability that may occur depending on the outcome of an uncertain future event. A contingent liability has to be recorded if the contingency is likely and the amount of the liability can be reasonably estimated. Both GAAP and IFRS require companies to record contingent liabilities.

How are contingencies handled by GAAP?

GAAP requires that you report contingent liabilities as unspecified expenses on the income statement. You must disclose all contingencies that could significantly alter the company’s estimated earnings. Explain any obscure or potentially misleading items in the footnotes.How do you account for loss contingencies?

Due to conservative accounting principles, loss contingencies are reported on the balance sheet and footnotes on the financial statements, if they are probable and their quantity can be reasonably estimated. A footnote can also be included to describe the nature and intent of the loss.

How do IFRS and GAAP differ in their approach to allowing reversals of inventory write downs?

Write Down Reversals GAAP requires that the value of an inventory asset or fixed asset be written down to its market value; GAAP also specifies that the amount of the write-down cannot be reversed if the market value of the asset subsequently increases. Under IFRS, the write-down can be reversed.

How are IFRS and GAAP similar?

Both US GAAP and IFRS recognize fixed assets when purchased, but their valuation can differ over time. US GAAP requires that fixed assets are measured at their initial cost; their value can decrease via depreciation or impairments, but it cannot increase.

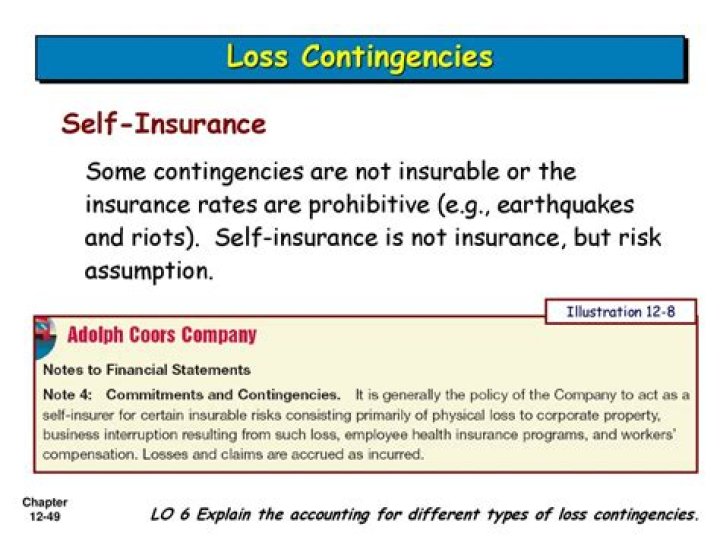

What is loss contingencies?

Loss Contingency. An existing condition, situation, or set of circumstances involving uncertainty as to possible loss to an entity that will ultimately be resolved when one or more future events occur or fail to occur.What is the definition of probable under IFRS under GAAP?

While a numeric standard for probable does not exist, practice generally considers an event that has a 75% or greater likelihood of occurrence to be probable. A provision must be probable to be recognized. Probable is interpreted as more likely than not (i.e., a probability of greater than 50 percent).

What is a contingent liability GAAP?Under GAAP, a contingent liability is defined as any potential future loss that depends on a “triggering event” to turn into an actual expense. … There are three GAAP-specified categories of contingent liabilities: probable, possible, and remote. Probable contingencies are likely to occur and can be reasonably estimated.

Article first time published onWhat distinguishes contingent liabilities from general uncertainties?

A potential obligation arising from a past event that may/may not result in future liabilities depending upon how future events occur. … These uncertainties are distinguished from contingent liabilities because they arise from future rather than past events.

How are provisions distinguished from contingent liabilities?

The key difference between a provision and a contingent liability is that provision is accounted for at present as a result of a past event whereas a contingent liability is recorded at present to account for a possible future outflow of funds.

What is equity under IFRS?

Equity is defined as “any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities” (IAS 32.11). Financial liabilities as defined under IAS 32 can be exceptionally classified as equity if they meet certain criteria: They are puttable instruments (IAS 32.16A and 16B).

Which of the following is an important characteristic of loss contingencies that is not commonly shared by other liabilities?

Which of the following is an important characteristic of loss contingencies that is not commonly shared by other liabilities? Uncertainty exists regarding whether a future event giving rise to the obligation will occur.

Which of the following is the proper treatment for a contingency that is probable but the exact amount of which is not known?

Which of the following is the proper treatment for a contingency that is probable but the exact amount of which is not known? The amount can be estimated. The liability should be estimated and recorded. Which of the following is required to be deducted from employees’ paychecks?

What two conditions need to exist for a contingent loss to require an accrual in the financial statements?

It requires accrual by a charge to income (and disclosure) for an estimated loss from a loss contingency if two conditions are met: (a) information available prior to issuance of the financial statements indicates that it is probable that an asset had been impaired or a liability had been incurred at the date of the …

What are the differences between IFRS and US GAAP for revenue recognition?

IFRS revenue recognition is guided by two primary standards and four general interpretations. GAAP, on the other hand, has highly specific rules and procedures codified for a huge variety of industries on a case-by-case basis. … Under IFRS rules, however, this is prohibited.

What is the difference between IFRS and Non IFRS?

Non-IFRS revenue measures have been adjusted from the respective IFRS financial measures by including the full amount of software support revenue, cloud revenue, and other similarly recurring revenue that we are not permitted to record as revenue under IFRS due to fair value accounting for the contracts in effect at …

What is the difference between US GAAP and Canadian GAAP?

Basically, US GAAP bases their accounting standards on the AICPA Accounting and Audit guide, whereas the Canadian GAAP bases their standards to their Accounting Guideline *8. … For US GAAP however, they only record the regular way purchases and other transactions of securities on a date of trade basis.

What is the difference between GAAP and accounting standards?

IFRSGAAPStands forInternational Financial Reporting StandardGenerally Accepted Accounting PrinciplesDeveloped by

What is the key difference between U.S. GAAP and IFRS in relation to the recording process quizlet?

IFRS requires comparative information to be disclosed with respect to the previous period for all amounts presented in the financial statements. US GAAP allows a single year presentation in certain circumstances and SEC rules require two years for the balance sheet and three years for all other statements.

How does IFRS differ from U.S. GAAP with respect to accounting for development costs?

GAAP tends to be more rules-based, while IFRS tends to be more principles-based. Under GAAP, companies may have industry-specific rules and guidelines to follow, while IFRS has principles that require judgment and interpretation to determine how they are to be applied in a given situation.

How IFRS define probable?

It is probable – i.e. more likely than not – that an outflow of resources (typically a payment) will be required to fulfil the obligation. The amount can be estimated reliably.

Which of the following is a difference between IAS 37 and US GAAP with respect to restructuring provisions?

IAS 37 does not allow recognition of a restructuring provision until a liability has been incurred. D.A restructuring provision and related loss is more likely to occur later under IAS 37 than under U.S. GAAP. A.U.S. GAAP does not allow recognition of a restructuring provision until a liability has been incurred.

What are provisions IFRS?

IFRS, the IAS 37 to be exact, defines provision as a liability of uncertain timing or amount. It means that, under the standard, those liabilities for which amount or timing of expenditure is uncertain, are deemed to be provisions.

What are the examples of loss contingency?

Loss Contingencies: a reduction in the value of an asset or an increase to a liability based on the outcome of a future event. Examples include obligations under a manufacturer’s warranty or a negative outcome from litigation.

What is the accounting treatment for a contingent liability?

Recording of Contingent Liabilities Contingent liabilities are never recorded in the financial statements of a company. These obligations have not occurred yet but there is a possibility of them occurring in the future. So a contingent liability has no accounting treatment as such.

What are examples of contingencies in accounting?

Injuries that may be caused by a company’s products, such as when it is discovered that lead-based paint has been used on toys sold by the business. The threat of asset expropriation by a foreign government, where compensation will be less than the carrying amount of the assets that will probably be expropriated.

What are contingent liabilities explain with example?

Description: A contingent liability is a liability or a potential loss that may occur in the future depending on the outcome of a specific event. Potential lawsuits, product warranties, and pending investigation are some examples of contingent liability.

How is contingent liability shown in balance sheet?

A contingent liability is recorded first as an expense in the Profit & Loss Account and then on the liabilities side in the Balance sheet.

What is contingent liability insurance?

What is contingent liability? Contingent liability, sometimes referred to as indirect liability, is a responsibility that occurs based on the outcome of a particular event that provides coverage for losses to a third party for which the insured is vicariously liable.