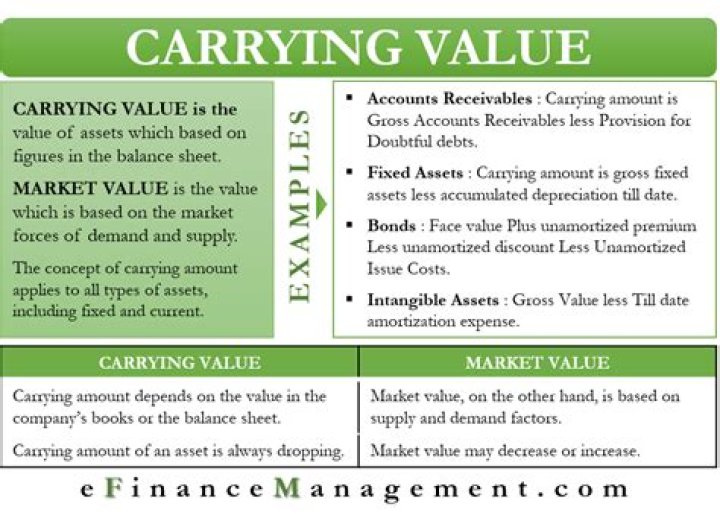

What is a carrying value in accounting

Carrying value is an accounting measure of value in which the value of an asset or company is based on the figures in the respective company’s balance sheet. For physical assets, such as machinery or computer hardware, carrying cost is calculated as (original cost – accumulated depreciation).

Is carrying value a liability?

What is the Carrying Amount? The carrying amount is the recorded cost of an asset, net of any accumulated depreciation or accumulated impairment losses. The term also refers to the recorded amount of a liability.

How do you calculate carrying value on a balance sheet?

It is calculated by taking the difference of the assets and liabilities on the balance sheet, also known as the Net Worth of the company; Calculated by multiplying the market price per share with the number of. Based on the historical cost of the asset.

What is the carrying value of the accounts receivable?

Examples of Carrying Amount Here are some examples when the term carrying amount or carrying value is used: A company’s Accounts Receivable has a debit balance of $84,000. The company’s Allowance for Doubtful Accounts has a credit balance of $3,000. The carrying amount or carrying value of the receivables is $81,000.What is the difference between book value and carrying value?

The term book value is derived from the accounting practice of recording an asset’s value based upon the original historical cost in the books minus depreciation. Carrying value looks at the value of an asset over its useful life; a calculation that involves depreciation.

What is the carrying value of a company?

The carrying value, or book value, is an asset value based on the company’s balance sheet, which takes the cost of the asset and subtracts its depreciation over time. The fair value of an asset is usually determined by the market and agreed upon by a willing buyer and seller, and it can fluctuate often.

Does carrying value include goodwill?

Goodwill impairment is an accounting charge that companies record when goodwill’s carrying value on financial statements exceeds its fair value. In accounting, goodwill is recorded after a company acquires assets and liabilities, and pays a price in excess of their identifiable net value.

What is carrying value of debt?

Definition: The carrying value of a bond is the par value or face value of that bond plus any unamortized premiums or less any unamortized discounts. The net amount between the par value and the premium or discount is called the carrying value because it is reported on the balance sheet.Why is carrying value important?

Importance of Book Value Book value is considered important in terms of valuation because it represents a fair and accurate picture of a company’s worth. … It means that investors and market analysts get a reasonable idea of the company’s worth.

Is carrying value the same as residual value?The residual value has increased to $9.000, due to increases in the prices of secondhand (used) vehicles. The depreciation charge for year 4 is reduced from $3.000 to $2.000, so the carrying value is the same as the residual value of $9.000. No change is made to depreciation charged in previous years.

Article first time published onHow is the carrying value of a stock calculated?

Divide the net assets available to common stock by the total number of shares outstanding to find the company’s carrying value per share. In this example, if the company has 40,000 shares outstanding, divide $400,000 by 40,000 shares to find the carrying value equals $10 per share.

How do you calculate carrying value of fixed assets?

- Take the original cost of purchasing the asset less salvage value.

- Divide that number by the number of years the asset is expected to be of use to generate the annual depreciation amount and record annually.

What is the carrying amount of inventory?

Inventory carrying cost is the total of all expenses related to storing unsold goods. The total includes intangibles like depreciation and lost opportunity cost as well as warehousing costs. A business’ inventory carrying costs will generally total about 20% to 30% of its total inventory costs.

What does IFRS 13 apply to?

Scope. IFRS 13 applies to all transactions and balances (whether financial or non-financial), with the exception of share-based payment transactions accounted for under IFRS 2, Share-based Payment, and leasing transactions within the scope of IAS 17, Leases.

What is the difference between NPV and NBV?

What is the definition of net book value? The NPV of an asset is essentially how much the asset is worth at a moment in time. … If the asset is damaged or sold and the organization is required to write-off or dispose of the asset, the NBV of the asset would be used to determine the impact to the financial statements.

How do you find the carrying value at the end?

The equation for calculating carrying value on most assets is simple. Take the original purchase cost. Add up the depreciation or amortization over the years you’ve held the asset and subtract the total from the purchase price. Then subtract any impairments on the value.

How do you find the carrying value of a reporting unit?

Under the Asset premise, the carrying value of the reporting unit is calculated as the sum of the carrying amounts of its assets less its deferred tax liabilities.

How is the carrying value of goodwill determined?

Goodwill is calculated by taking the purchase price of a company and subtracting the difference between the fair market value of the assets and liabilities. Companies are required to review the value of goodwill on their financial statements at least once a year and record any impairments.

What is goodwill example?

Goodwill is an intangible asset associated with the purchase of one company by another. … The value of a company’s brand name, solid customer base, good customer relations, good employee relations, and any patents or proprietary technology represent some examples of goodwill.

What is the gross carrying amount of an asset?

According to the provisions of Appendix A – Defined terms of IFRS 9, the gross carrying amount of a financial asset is the amortised cost of the financial assets, before adjusting for any loss allowance.

Is face value the same as carrying value?

Carrying value is the combined total of a bond’s face value and any unamortized discounts or premiums. … These discounts are gradually amortized over the life of the bond, so that by the maturity date of a bond, its face value equals its carrying value.

How is Pb ratio calculated?

The price-to-book ratio (P/B) is calculated by dividing a company’s market capitalization by its book value of equity as of the latest reporting period. Alternatively, the P/B ratio can be calculated by dividing the latest closing share price of the company by its most recent book value per share.

What is book capitalization?

In finance, capitalization refers to the book value or the total of a company’s debt and equity. Market capitalization is the dollar value of a company’s outstanding shares and is calculated as the current market price multiplied by the total number of outstanding shares.

What is the carrying value of a note?

The carrying amount of an interest bearing note is equal to the note’s face value less any repayments on the note made over its lifetime.

Does carrying amount include accrued interest?

The carrying amount of financial instruments shall include accrued interest.

How is PNL bond calculated?

Multiply the par price of the bond by the interest it is paying. If the par price is $1,000 and the interest is 5 percent, that yields $50 each year. Multiply the interest earned per year by the years to maturity on the bond. In this example, if there are 10 years remaining, that is $500.

What is residual value example?

For example, residual may be expressed this way: $30,000 MSRP * Residual Value of 50% = $15,000 value after 3 years. So, a car with an MSRP of $30,000 and a residual value of 50% after three years would be worth $15,000 at the end of its lease.

What is net carrying amount?

Net carrying amount refers to the current recorded balance of an asset or liability, netted against the amount in the contra account with which it is paired. For example, a fixed asset has a current recorded balance of $50,000, and there is $10,000 of accumulated depreciation in the contra account with which it paired.

What are the reasons for carrying inventory?

- Meet variation in Production Demand. …

- Cater to Cyclical and Seasonal Demand. …

- Economies of Scale in Procurement. …

- Take advantage of Price Increase and Quantity Discounts. …

- Reduce Transit Cost and Transit Times.

What are the 3 levels of fair value?

Definition. The Fair Value Hierarchy categorises the inputs used in Valuation techniques into three levels. The hierarchy gives the highest priority (Level 1) to (unadjusted) quoted prices in active markets for identical assets or liabilities and the lowest priority (Level 3) to unobservable inputs.

What are Level 2 assets?

Level 2 assets are financial assets and liabilities that do not have regular market pricing, but whose fair value can be determined based on other data values or market prices. … Level 2 assets are commonly held by private equity firms, insurance companies, and other financial institutions with investment arms.