What is coverage D on a homeowners policy

Loss of use coverage, also known as additional living expenses (ALE) insurance, or Coverage D, can help pay for the additional costs you might incur for reasonable housing and living expenses if a covered event makes your house temporarily uninhabitable while it’s being repaired or rebuilt.

What is coverage type D?

Coverage D: Additional Living Expense. Covers additional living expenses when incurred.

What are the 3 basic levels of coverage that exist for homeowners insurance?

Homeowners insurance policies generally cover destruction and damage to a residence’s interior and exterior, the loss or theft of possessions, and personal liability for harm to others. Three basic levels of coverage exist: actual cash value, replacement cost, and extended replacement cost/value.

How much is D coverage?

Coverage D is normally limited to 20 percent of Coverage A. In the event of a loss it is important that you keep receipts for all additional living expenses and submit them to your company for reimbursement consideration.Which statement is true concerning coverage D of the homeowners policy?

Which statement is true concerning Coverage D of the Homeowners Policy? The coverage will pay for any increase in living expenses required to maintain the insured’s normal standard of living – Coverage D is intended to pay only the increase in the insured’s normal living expenses occasioned by the loss.

What are the five basic areas of coverage on a homeowners insurance policy?

[Voiceover] Want to learn about homeowners insurance? In short, homeowners insurance helps protect you, your home and your belongings from a variety of unexpected events. A standard policy includes four key types of coverage: dwelling, other structures, personal property and liability.

Do I have to insure my home for replacement cost?

In the event of a loss, replacement cost coverage gives your family the best chance to return to their home and usual quality of life with minimal financial interruption. For the best protection, experts recommend that you insure your home for at least 100 percent of its estimated replacement cost.

What is not usually covered by homeowners insurance?

What Standard Homeowner Insurance Policies Don’t Cover. Standard homeowners insurance policies typically do not include coverage for valuable jewelry, artwork, other collectibles, identity theft protection, or damage caused by an earthquake or a flood.What is coverage G?

Coverage G — Barns, Outbuildings and Other Farm Structures provides coverage for the following scheduled items or classes of property: Farm Barns. … Building materials and supplies for use in building, altering or repairing farm buildings or structures provided that they are kept on or adjacent to the insured location.

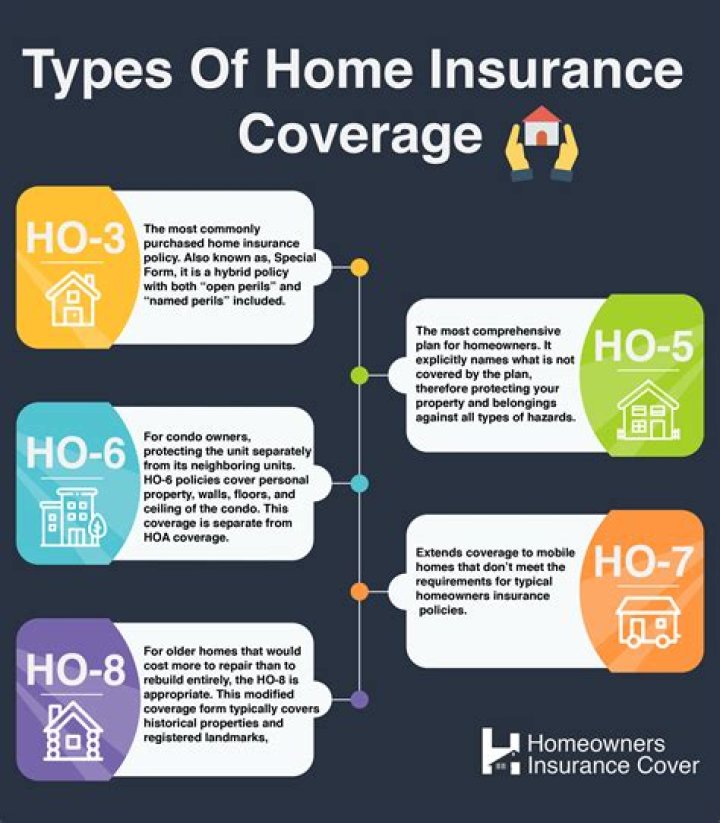

What is the most important part of homeowners insurance?The most important part of homeowners insurance is the level of coverage. Avoid paying for more than you need. Here are the most common levels of coverage: HO-2 – Broad policy that protects against 16 perils that are named in the policy.

Article first time published onHow much should my house be insured for?

Most homeowners insurance policies provide a minimum of $100,000 worth of liability insurance, but higher amounts are available and, increasingly, it is recommended that homeowners consider purchasing at least $300,000 to $500,000 worth of liability coverage.

Which of the following homeowners coverage does not have a deductible?

Which of the following homeowners coverage does not have a deductible? Damage to property of Others is an Additional Coverage under Section II, which is not subject to a deductible. A guest falls in K’s house and is injured in an amount of $1,000.

What is the difference between vandalism and malicious mischief?

Vandalism is damage done to someone else’s property, simply for the sake of causing damage. … Malicious mischief is similar, though the damage may not have been intended.

Which claim would be covered under Coverage E of a homeowners policy?

The Coverage E—Personal Liability Coverage provisions provide coverage if a claim is made or a suit is brought against an insured because of bodily injury or property damage arising from a covered occurrence.

How much dwelling coverage should you have?

Most lenders require you to have dwelling coverage limits of either 20% of the value of your condo or $100 per square foot for your condo.

How do you determine the replacement cost of your home?

Home replacement cost is the total amount required to rebuild your home to its original standard. Your dwelling limit must be at least 80% of your home’s rebuild value to be fully covered. Home replacement cost can be calculated by multiplying your area’s average per-foot rebuilding cost by your home’s square footage.

Can you insure your house for more than it is worth?

When you insure-to-value, some carriers will automatically provide extended replacement cost. If it costs more to rebuild the home than originally estimated, this type of policy will provide coverage above and beyond the amount of coverage, ranging from 125% to unlimited coverage (depending on your state and insurer).

What is covered under Coverage A?

“Coverage A” on a Homeowners insurance policy covers damage to your home’s structure. … Coverage A must cover the cost of rebuilding your home at current construction costs. This doesn’t include the cost of the land your home sits on. Coverage A is not the market value of your home or the amount you paid for it.

What types of insurance are not recommended?

- Mortgage Life Insurance. There are some insurance agents that will try to convince you that you need mortgage life insurance. …

- Identity Theft Insurance. …

- Cancer Insurance. …

- Payment protection on your credit card. …

- Collision coverage on older cars.

What are the six categories covered by homeowners insurance?

- Property Damage. This covers damage to your home , such as from fire, wind, or hail. …

- Additional Living Expenses. …

- Personal Liability. …

- Medical Payment Coverage.

What is Coverage A and B?

In general, Coverage A covers damage to the dwelling or house. Coverage B covers damage to other structures such as a detached garage, work sheds, etc.

What is coverage H?

Coverage H — Farm Liability Coverage – Bodily Injury & Property Damage Liability coverage is provided for the sums that the insured becomes legally obligated to pay (up to the policy limit) as damages because of bodily injury or property damage to which the insurance applies.

What are 2 things not covered in homeowners insurance?

Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered. Damage caused by smog or smoke from industrial or agricultural operations is also not covered. If something is poorly made or has a hidden defect, this is generally excluded and won’t be covered.

Is wind damage covered by homeowners insurance?

Yes, as noted above, homeowners insurance typically covers most types of wind damage. Usually, the dwelling coverage of your homeowners policy will help pay to repair or replace damage to the roof, siding or windows due to a wind event.

Does homeowners insurance cover water damage from a leaking roof?

Homeowners insurance covers water damage from a leaking roof when a covered peril — such as a sudden storm, faulty installation or accidental cracking — caused the leak. This means that if your shingles weren’t installed correctly or broke off accidentally, any water damage caused by a leaking roof would be covered.

How much is homeowners insurance on a $200000 house?

Estimated Home ValueAverage annual premiums for an HO-3 Policy$150,000 to $174,999$981$175,000 to $199,999$1,018$200,000 to $299,999$1,114$300,000 to $399,999$1,272

How much is homeowners insurance on a $300000 house?

Average rateDwelling coverageLiability$1,806$200,000$100,000$1,824$200,000$300,000$2,285$300,000$100,000$2,305$300,000$300,000

Does home insurance cover damage to other people's property?

Homeowners insurance is a package policy. This means that it covers both damage to property and liability or legal responsibility for any injuries and property damage policyholders or their families cause to other people.

What is it called when someone damages your property?

Criminal mischief has likely been around for as long as people have owned personal property. … Criminal mischief is also known as malicious mischief, vandalism, damage to property, or by other names depending on the state.

What is the penalty for malicious mischief?

Under Vehicle Code 10853 VC, malicious mischief is a misdemeanor offense. As such, it is punishable by: Imprisonment in the county jail for up to six months; and/or, A fine of up to $1,000.

Can you damage your own property?

An owner can damage his or her own property if, at the same time, it belongs to someone else within the meaning of section 10 (2) of the Act.