What is the journal entry of accrued expenses

Usually, an accrued expense journal entry is a debit to an Expense account. The debit entry increases your expenses. You also apply a credit to an Accrued Liabilities account.

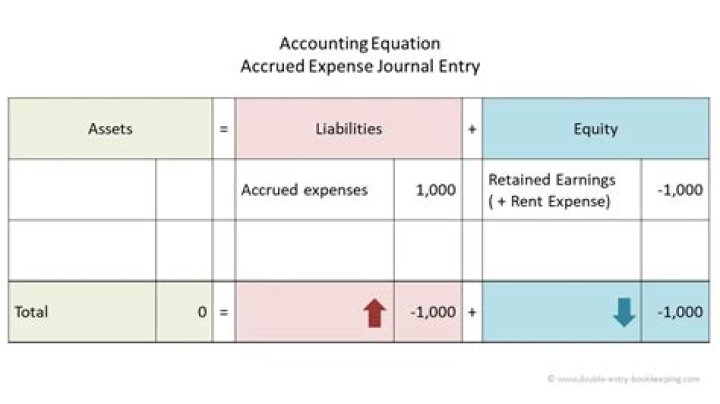

How is accrued expenses recorded?

Accrued expenses or liabilities occur when expenses take place before the cash is paid. The expenses are recorded in a company’s balance sheet. The financial statements are key to both financial modeling and accounting.

What is the journal entry for accrued liabilities?

The journal entry for an accrued liability is typically a debit to an expense account and a credit to an accrued liabilities account. At the beginning of the next accounting period, the entry is reversed.

What is an example of an accrued expense?

Examples of accrued expenses include: Utilities used for the month but an invoice has not yet been received before the end of the period. Wages that are incurred but payments have yet to be made to employees. Services and goods consumed but no invoice has been received yet.Why do we record accrued expenses?

Since accrued expenses represent a company’s obligation to make future cash payments, they are shown on a company’s balance sheet as current liabilities. … Following the accrual method of accounting, expenses are recognized when they are incurred, not necessarily when they are paid.

Where are accrued expenses recorded?

You record an accrued expense when you have incurred the expense but have not yet recorded a supplier invoice (probably because the invoice has not yet been received). Accrued expenses tend to be short-term, so they are recorded within the current liabilities section of the balance sheet.

How do you record accrued expenses on a balance sheet?

Accrued Expenses on Balance Sheet Accordingly, it should be recorded by debiting Wages and Salaries Expenses and crediting Accrued Expenses and by making an offsetting entry by debiting these expenses and crediting Cash when payment is made.

How do I enter an accrued expense in Quickbooks?

- Go to the + New menu and select Bill.

- From the Vendor dropdown, select a vendor.

- From the Terms dropdown, select the bill’s terms. …

- Enter the Bill date, Due date, and Bill no. …

- Enter the bill details in the Category details section. …

- Enter the Amount and tax.

How do you record accrued revenue journal entry?

On the financial statements, accrued revenue is reported as an adjusting journal entry under current assets on the balance sheet and as earned revenue on the income statement of a company. When the payment is made, it is recorded as an adjusting entry to the asset account for accrued revenue.

How do you model Accrued expenses?Accrued Expenses: Take the average of Accrued Expenses/Sales from Years 1 through 3, which is 8%, and keep that percentage constant in the forecasted years. (Again, we can add increments or decrements to this number in future years if we feel it is appropriate.)

Article first time published onIs accrued expenses an expense account?

Accrued expenses are expenses a company accounts for when they happen, as opposed to when they are actually invoiced or paid for. An accrual method allows a company’s financial statements, such as the balance sheet and income statement, to be more accurate.

When can you accrue an expense?

In short, accruals allow expenses to be reported when incurred, not paid, and income to be reported when it is earned, not received. As examples: A department orders and receives tow computers at the end of June 2004. However, the bill is not received Until July and is not processed until August.

What is the accounting entry for the accrual of wages?

Accrued wages are recorded in order to recognize the entire wage expense that a business has incurred during a reporting period, not just the amount actually paid. The accrued wages entry is a debit to the wages expense account, and a credit to the accrued wages account.

How do you clear accrued expenses?

Reversing Accrued Expenses When you reverse an accrual, you debit accrued expenses and credit the expense account to which you recorded the accrual. When you post the invoice in the new month, you typically debit expenses and credit accounts payable.

Does QuickBooks do accrual accounting?

Yes, you can simply record your transactions inside QuickBooks as normal. Then, run your reports as Accrual or Cash to show your income or expenses. … On the other hand, the Accrual basis shows the income and expenses based on when you sent your invoices or got your bills.

How do I set up an accrual in QuickBooks?

- Log in to your file as the Administrator. Make sure you are in Single-User Mode.

- Go to the Edit menu, then select Preferences.

- Select Reports & Graphs, then go to the Company Preferences tab.

- In the Summary Report Basis section, select Accrual or Cash.

- Select OK.

What is an accrued liability account?

An accrued liability occurs when a business has incurred an expense but has not yet paid it out. Accrued liabilities arise due to events that occur during the normal course of business. These liabilities or expenses only exist when using an accrual method of accounting.

What expenses should be accrued?

- Bonuses, salaries or wages payable.

- Unused vacation or sick days.

- Cost of future customer warranty payments, returns or repairs.

- Unpaid, accrued interest payable.

- Utilities expenses that won’t be billed until the following month.

What is the 3 statement model used for?

The purpose of a 3-statement model (i.e. an integrated financial statement model) is to forecast or project the financial position of a company as a whole. It contains the three types of financial statements – balance sheet, income, and cash flow statement – which are linked together.

Is accrued salaries an expense?

The accrued salaries are the amount of salary expenses for which the employees have done work, but it has not been paid yet by the business. This issue occurs when businesses are most likely to pay their employees on a certain date, but this date may not include all the work done until the end of the accounting period.

What is reversal journal entry?

Reversing entries, or reversing journal entries, are journal entries made at the beginning of an accounting period to reverse or cancel out adjusting journal entries made at the end of the previous accounting period.