What is the maximum loan to value for a cash out refinance

Mortgage lenders usually allow cash out up to 80% of the property value, but FHA allows 85% and the VA allows 100%. When refinancing to access cash, your loan may not exceed a maximum loan-to-value ratio. That means your total home debt can’t exceed a certain percentage of the value of your home.

What is the maximum LTV for a cash-out refinance?

Lenders also use your loan-to-value ratio (LTV) to evaluate your eligibility for a cash-out refinance. Your LTV is the comparison of your mortgage amount to the value of your home. Some lenders won’t allow homeowners to exceed an 80% LTV to secure a cash-out refinance.

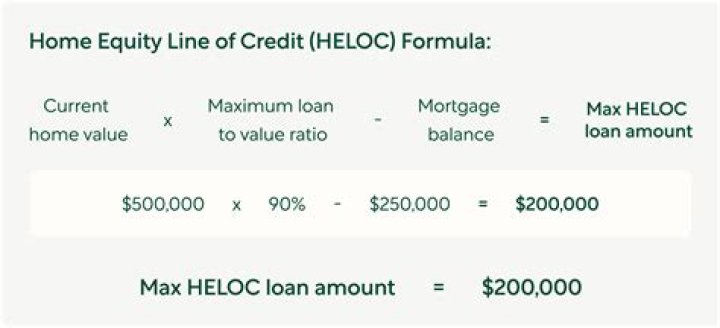

What is the max LTV for a Heloc?

The amount of equity you currently have in your home will determine your Home Equity Line of Credit (HELOC) limit. You must retain at least 10% of the value of the equity in your home (sometimes referred to as a 90% LTV maximum).

Can I refinance at 90 LTV?

You can refinance with as little as 3.5 percent equity — a 96.5 percent loan-to-value — with a Federal Housing Administration loan in which the government insures the lender against default. … Typically, you need at least 10 percent equity — a 90 percent LTV to refinance with a conventional loan.Can you refinance 95 LTV?

There is a huge opportunity for homeowners because they can now refinance their mortgage up to 95% of the appraised value of the home and with NO PMI (private mortgage insurance).

Do you need 80 equity to refinance?

For conventional refinances, you’ll need at least 20 percent equity in your home to avoid private mortgage insurance, or PMI. This also means you generally need a loan-to-value (LTV) ratio of no more than 80 percent. You can use Bankrate’s LTV calculator to find out your ratio.

How much equity do I need to refinance with cash out?

Borrowers generally must have at least 20 percent equity in their homes to be eligible for a cash-out refinance or loan, meaning a maximum of 80 percent loan-to-value (LTV) ratio of the home’s current value.

What percentage of your home equity can you borrow against?

A home equity loan generally allows you to borrow around 80% to 85% of your home’s value, minus what you owe on your mortgage. You can do some simple math to estimate how much you might be able to borrow.What is the max LTV on an investment property?

What is the max LTV on an investment property? You need at least a 15–20% down payment to buy an investment property. That means the max LTV is 80–85%. For an investment property cash out refinance, the max LTV is 70–75% depending on your lender and whether the loan is fixed–rate or adjustable–rate.

Can you borrow 100 home equity?To qualify for a home equity loan, in many cases, your loan-to-value (LTV) ratio — the percentage of your home’s value being financed by a first and/or second mortgage — shouldn’t exceed 85%. However, it’s possible to get a high-LTV home equity loan that allows you to borrow up to 100% of your home’s value.

Article first time published onHow is LTV calculated for Heloc?

To figure out your LTV ratio, divide your current loan balance (you can find this number on your monthly statement or online account) by your home’s appraised value. Multiply by 100 to convert this number to a percentage.

What is Hiro loan?

HIRO is short for “high LTV refinance option” — a special refi program run by Fannie Mae. If you have very little equity, but want to refinance into today’s low mortgage rates, you might be able to use this loan to your advantage. It could help lower your rate and make your monthly mortgage payment more affordable.

Do 95 mortgages still exist?

There’s a number of lenders now offering 95% mortgages under the government-backed mortgage guarantee scheme. The scheme will run until 31 December 2022, so you’ll need to get your application in by then.

Do banks give 95 mortgages?

Lenders (banks and building societies) will be encouraged to offer 95% mortgages based on the government guaranteeing outstanding loans.

Can I sell my house after a cash-out refinance?

You can sell your house right after refinancing — unless you have an owner-occupancy clause in your new mortgage contract. An owner-occupancy clause can require you to live in your house for 6-12 months before you sell it or rent it out.

Why is my loan amount higher after refinancing?

Home loan interest is tipped toward the early years. … If you’ve had your loan for a while, more money is going to pay down principal. If you refinance, even at the same face amount, you start over again, initially paying more on interest. That, in effect, increases your mortgage.

Do you pay taxes on refinance cash out?

The cash you collect from a cash-out refinancing isn’t considered income. Therefore, you don’t need to pay taxes on that cash. … For example, you’re allowed to deduct the interest on the original loan if money from the cash-out refinance goes toward permanent improvements that boost the value of your home.

What is a limited cash-out refinance?

What is a limited cash-out refinance? A limited cash-out refinance replaces an existing mortgage with a new one, but the new loan amount is slightly larger. This is because the refinancing costs are added to the balance instead of the borrower paying them out of pocket.

What is a limited cash out refinance Fannie Mae?

What is a limited cash-out refinance? A limited cash-out refinance replaces your existing mortgage loan with a new loan having a lower interest rate, shorter term, or both. … Per Fannie Mae’s rules, the cash-back amount is limited to 2% of the new loan balance or $2,000, whichever is less.

How do you calculate cash-out refinance?

Keeping the maximum 80% LTV ratio requirement in mind, you may borrow up to an additional $60,000 with a cash-out refinance. To calculate this, multiply your home’s value by 80% ($200,000 x 0.80 = $160,000) and subtract your outstanding loan balance from that amount ($160,000 – $100,000 = $60,000).

How can I get the equity out of my home without selling it?

Home equity loans, home equity lines of credit (HELOCs), and cash-out refinancing are the main ways to unlock home equity. Tapping your equity allows you to access needed funds without having to sell your home or take out a higher-interest personal loan.

Does a home equity loan require an appraisal?

In a word, yes. The lender requires an appraisal for home equity loans—no matter the type—to protect itself from the risk of default. If a borrower can’t make his monthly payment over the long-term, the lender wants to know it can recoup the cost of the loan. An accurate appraisal protects you—the borrower—too.

What is the monthly payment on a $200 000 home equity loan?

On a $200,000, 30-year mortgage with a 4% fixed interest rate, your monthly payment would come out to $954.83 — not including taxes or insurance.

How much is a $50000 home equity loan payment?

Loan payment example: on a $50,000 loan for 120 months at 3.80% interest rate, monthly payments would be $501.49.

What is the monthly payment on a $100 000 home equity loan?

Assuming principal and interest only, the monthly payment on a $100,000 loan with an APR of 3% would come out to $421.60 on a 30-year term and $690.58 on a 15-year one. Credible is here to help with your pre-approval.

How do you calculate loan to value for refinance?

- Current loan balance ÷ Current appraised value = LTV.

- Example: You currently have a loan balance of $140,000 (you can find your loan balance on your monthly loan statement or online account). …

- $140,000 ÷ $200,000 = .70.

- Current combined loan balance ÷ Current appraised value = CLTV.

What is a high LTV loan?

A high-ratio loan usually means the loan-to-value (LTV) exceeds 80% of the property’s value and may approach 100% or higher. Mortgage loans that have high loan ratios can be quite risky, and carry above-average interest rates.

What is the Freddie Mac Enhanced Relief refinance Program?

Freddie Mac’s Enhanced Relief Refinance program was created to help borrowers with very little equity refinance into a lower rate and monthly payment. Typically, homeowners need a certain amount of home equity to qualify for a refinance. You build equity as you pay down your mortgage and as the home’s value increases.

Who qualifies for Hero program?

Eligibility requires homeowners to have at least 10% equity in their home, are current with the property taxes and mortgage payments, have not recently filed for bankruptcy, and the products are approved for this type of loan.

Can I get a 5% deposit?

To qualify for a 5% deposit mortgage backed by the government guarantee you must meet certain criteria: You must have a deposit of between 5% and 9% Any homebuyer can apply for a mortgage, not just first-time buyers. Unlike the Help to Buy shared scheme, the property does not have to be a new-build home.

Can you get a mortgage on benefits?

Yes! Getting a mortgage while on benefits is certainly possible under the right circumstances. The chances of your application being approved are likely to hinge on whether you have other income or assets in addition to the money you’re getting through benefits.