What are the 3 types of net asset restrictions

Businesses classify net assets in three categories: unrestricted, temporarily restricted and permanently restricted.

What are the three types of net asset restrictions?

Classes of Net Assets Presently nonprofits use three net asset classifications: Unrestricted. Temporarily restricted. Permanently restricted.

What are the three categories into which not for profits must classify their net assets?

13. A statement of financial position provided by a not-for-profit organization shall report the amounts for each of three classes of net assets—permanently restricted net assets, temporarily restricted net assets, and unrestricted net assets—based on the existence or absence of donor-imposed restrictions.

What are the 3 types of donor-imposed restrictions?

- Purpose-restricted: These are funds that are donor-restricted for use on a particular project.

- Time-restricted: These are funds that are donor-restricted for use in a certain time period.

What is net assets from restrictions?

Net assets released from restrictions refers to those restricted assets that have been re-classified as unrestricted net assets. This transfer occurs because the original donor-imposed restrictions associated with certain assets have been satisfied.

How do you classify restricted funds?

- Temporarily Restricted. A temporarily restricted fund is usually time-bound and can be used for a specific purpose within a specified period. …

- Permanently Restricted.

What are the net assets of a company?

Net assets are the value of a company’s assets minus its liabilities.

What are unrestricted net assets?

Unrestricted net assets are donations to nonprofit organizations that can be used for general expenses or any other legitimate purpose of the nonprofit. Temporarily restricted net assets are usually earmarked by the donor for a specific program or project and must be used within a set time period.What are donor restrictions?

Donors to a nonprofit organization may designate—or restrict—the use of their donations to a particular purpose or project. An example is a gift to a special scholarship fund at a university. Unrestricted funds are donations the nonprofit may use for any purpose.

What is a donor imposed restriction?Either a temporary restriction or a permanent restriction imposed by the donor of an asset when it is contributed to a nonprofit organization.

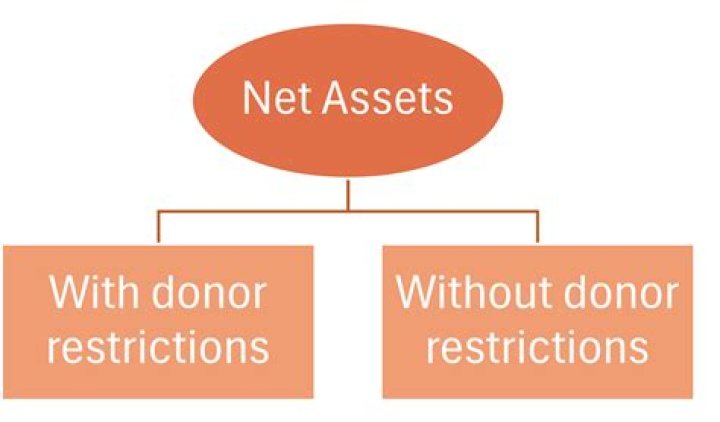

Article first time published onWhat are the two categories into which NFPs must classify their net assets?

The two different categories that NFPs must classify their net assets into are with donor restrictions, and without donor restrictions. Any asset with donor restrictions have to be put towards a specific purpose.

How are net assets required to be classified on Not for Profits financial statement?

Net assets are categorized based on the existence or absence of donor restrictions. Unrestricted net assets do not have any restrictions on how your organization can use those funds. Restricted net assets come with specific donor-imposed stipulations or conditions.

Are unrestricted net assets retained earnings?

Unrestricted net assets, which is the retained earnings account 2. Temp Restricted Net Assets for temporarily restricted net assets, 3. Perm Restricted Net Assets for permanently restricted net assets, also called endowment.

What are board designated net assets?

The term “board-designated assets” generally refers to funds that have not been restricted by donors but are subject to self-imposed limits on their use. They are typically intended to ensure that funding is available when needed.

In which classification of net assets are expenses reported?

An expense is reported in the unrestricted column of the statement of activities, unrestricted net assets are increased, and temporarily restricted net assets are decreased.

Are net assets released from restrictions revenue?

They are reported as a separate line or lines on the face of the statement of activities using a caption such as “net assets released from restriction.” Because releases of restriction are not considered revenue, financial statement subtotals that include increases of net assets associated with releases of restriction …

What are examples of net assets?

Example: If a company claims $11,000,0000 in assets and $6,000,000 in liabilities on a balance sheet, the net assets would be $11,000,000 – $6,000,000 = $5,000,000 in net assets.

What is net asset method?

What Is the Adjusted Net Asset Method? The adjusted net asset method is a business valuation technique that changes the stated values of a company’s assets and liabilities to reflect its estimated current fair market values better. … This method may also be called the asset accumulation method.

What do net assets show?

Net assets are what a company owns outright, minus what it owes. Put another way, net assets equal the company assets (economic resources) minus liabilities (what is owed to someone else). … Net assets are virtually the same as shareholders’ equity because it’s the company’s monetary worth.

What's the difference between restricted and unrestricted funds?

Definition. Restricted funds are monies set aside for a particular purpose as a result of designated giving. They are permanently restricted to that purpose and cannot be used for other expenses of the nonprofit. By contrast, unrestricted funds may be used for any legal purpose appropriate to the organization.

What is the difference between restricted and designated funds?

Designated funds – these are unrestricted funds that the trustees have set aside for a particular purpose. … Restricted funds – restricted funds have been given to a charity for a particular purpose and can only be spent on that purpose.

What does restricted funds mean in accounting?

Restricted funds are funds subject to specific trusts, which may be declared by the donor(s) or with their authority (e.g. in a public appeal) or created through legal process, but still within the wider objects of the charity.

What is a purpose restriction?

One of the types of donor-imposed temporary restrictions. An example of a purpose restriction is a cash donation with a donor-imposed requirement that the money be used only to purchase a vehicle for one of its programs.

What are restricted reserves?

Restricted funds may be restricted income funds, which are spent at the discretion of the trustees in furtherance of some particular aspect(s) of the objects of the charity, or they may be endowment funds, where the assets are required to be invested, or retained for actual use, rather than spent.

What are endowments?

In general, an endowment is a donation of money or property to a non-profit organization, which uses the resulting investment income for a specific purpose.

What is the difference between stockholders equity and net assets or unrestricted net assets?

The balance sheet is called the statement of financial position. The income statement is the statement of activities. Shareholder equity is replaced with net assets. … Net assets is more descriptive, implying that the number represents the net difference between the non-profit’s assets and its liabilities.

Can restricted net assets be negative?

Put another way, net assets is the amount of the organization’s assets not financed with debt. It’s even possible, if liabilities exceed assets, for net assets to be negative. Negative net assets would be bad.

What are temporary restricted net assets?

Temporarily Restricted assets are those items donated to the organization that was received with some kind of restriction placed on them by the donor, that will be fulfilled in the near future (usually within one year).

How do you record a release from restrictions?

The journal entry is to debit a “Release of Restriction — Temporarily Restricted” account and credit “Release of Restriction — Unrestricted” account. Note that the revenue account is not touched when revenues are released — release accounts are used instead.

What restrictions donors may impose on the use of resources they contribute to a not for profit organization?

Restrictions donors may impose on the use of resources they contribute to NFPOs. Temporary restriction-donation must be used for a specific purpose, such as a special training program; restriction satisfied when money is spent for purpose. Also when gift may be used.

What is a time restricted grant?

Temporarily restricted funds are restricted for a particular period of time and can be used for donor desired purposes within the period. Like, a fund designated to use for a specific event is restricted until the event is finished. After that, the fund becomes unrestricted.